MITI's CBU EV Ruling Will Wipe Out These EV Brands

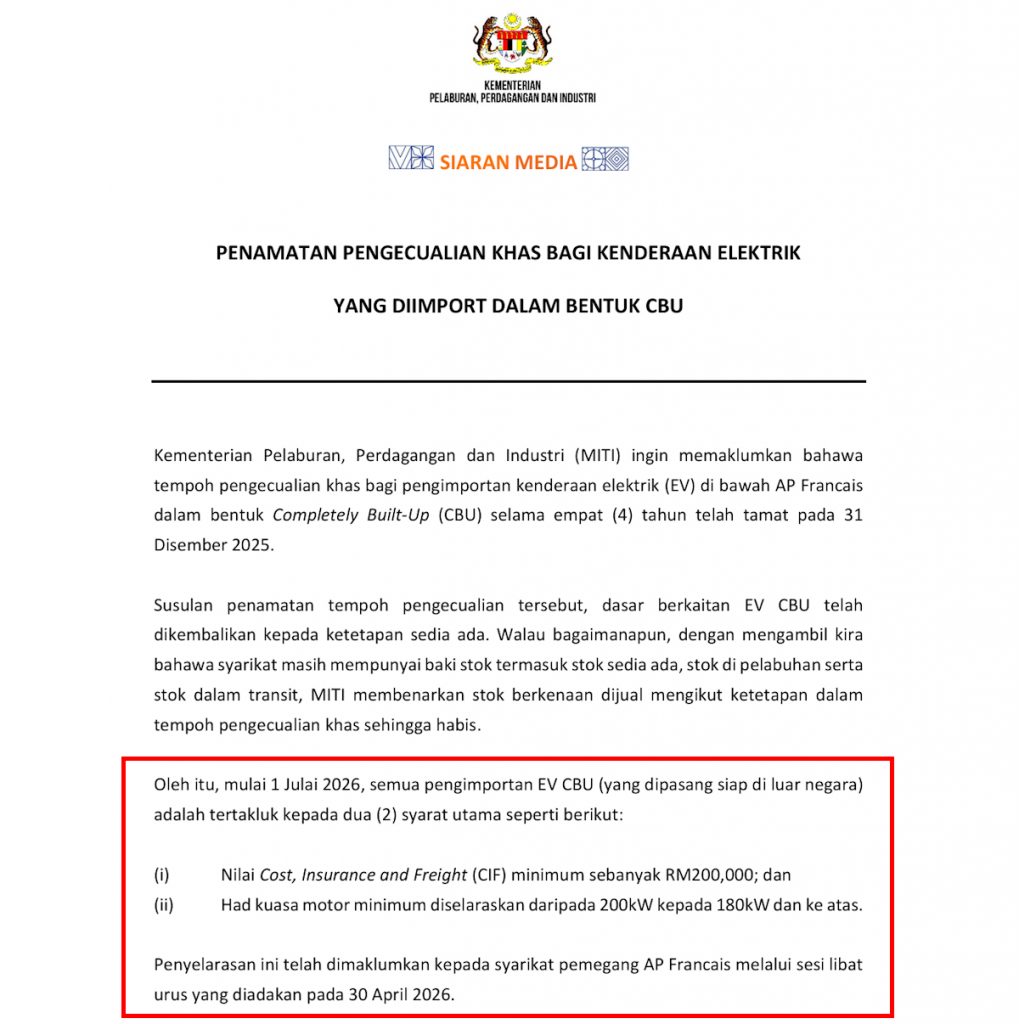

Malaysia’s electric vehicle market is undergoing its most aggressive regulatory reset to date. Effective 2026, the Ministry of International Trade and Industry is eliminating the tax holidays and import allowances that have long supported fully assembled battery electric vehicles, creating an immediate ultimatum for global manufacturers. MITI's new CBU EV ruling will wipe out electric vehicles from BYD, GWM, Toyota, Smart, Mini, iCaur, BMW, Tesla, Honda, Nissan, MG, Zeekr and more in Malaysia. Any brand unwilling or unable to transition to local assembly will effectively lose access to one of Southeast Asia’s most critical automotive markets. The directive ends the era of direct CBU imports and establishes a hard requirement for domestic production partnerships or wholly owned assembly plants. For a market that has relied on imported zero-emission vehicles to jump-start adoption, the policy represents a sudden divorce from the global supply chain.

The End of the CBU Import Era

For the past several years, Malaysia has relied on a hybrid incentive structure that allowed both locally assembled and fully imported EVs to benefit from duty exemptions under the National Automotive Policy. That equilibrium is now over. Under the revised framework, MITI will restrict Approved Permits and revoke tax waivers for CBU electric models, stripping imported units of the price advantage that made them competitive against internal combustion vehicles. Previously, imported EVs enjoyed full exemptions from import duties, excise duties, and sales taxes, often resulting in showroom prices 30 to 40 percent lower than conventionally taxed vehicles. Those savings are about to vanish.

The move is designed to accelerate industrial localization. By forcing automakers to establish CKD operations, the government aims to develop a domestic EV supply chain, create skilled manufacturing jobs, and ensure that long-term value remains inside Malaysia rather than flowing to overseas factories. For consumers, however, the short-term effect will be reduced choice and immediate pricing pressure on remaining inventory. Analysts predict that the average sticker price for a non-localized EV could climb by $10,000 to $15,000 USD once full tariffs are applied, effectively freezing demand for imported nameplates.

Which Brands Face Immediate Discontinuation

Mass-Market Chinese and Regional Players

Chinese manufacturers have dominated Malaysia’s budget and mid-range EV segments by flooding the market with aggressively priced CBU units. BYD, which moved substantial volume through the Atto 3 and Seal, lacks a localized assembly timeline and now faces a complete portfolio withdrawal. Great Wall Motor and its subsidiaries, including Ora and tank brands under the GWM umbrella, are similarly exposed. MG and Zeekr, which entered Malaysia on the back of direct import strategies, will see their distribution networks collapse without swift factory partnerships.

iCaur, a newer entrant that bet heavily on CBU logistics to keep showroom prices under RM 100,000 (approximately $21,000 USD), no longer has a viable path to profitability under the ruling. The brand’s entire business case relied on bypassing local assembly overhead, a model that MITI has now rendered obsolete. Without the capital reserves to build a plant or the volume to justify one, these value-focused marques are the most likely to execute a full retreat.

Premium and Legacy Global Automakers

The disruption extends well beyond value-oriented marques. BMW and Mini, which import their i-series and Electric Cooper SE as fully built units, must now fast-track CKD negotiations or cede premium EV share to locally assembled competitors. Smart, operated as a joint venture but historically dependent on European and Chinese CBU supply, faces an identical restructuring requirement. The cost of localizing premium niche models with low annual sales volume rarely pencils out, which means many of these nameplates will be discontinued regardless of corporate willingness to stay.

Tesla, which established a direct-sales presence in Malaysia without local manufacturing, now confronts a closed market unless it commits to domestic assembly. Legacy Japanese giants including Toyota, Honda, and Nissan are also caught in the transition; their initial EV crossovers were brought in as low-volume CBU offerings to test demand. Without retooling for CKD, those nameplates will vanish from Malaysian showrooms. The ruling effectively punishes every legacy strategy that treated Malaysia as a destination for finished goods rather than a manufacturing hub.

The CKD Mandate and Barriers to Entry

Transitioning from CBU to CKD is not a simple logistics change. It requires stamping facilities, battery pack assembly lines, paint shops, and localized supplier networks. The capital outlay easily exceeds $150 million USD for a basic operation, with full-scale plants demanding twice that investment. Smaller brands that lack the balance sheet or production volume to justify such spending will simply exit rather than comply. Even for deep-pocketed conglomerates, the eighteen-month timeline to regulatory enforcement leaves little room for construction delays or permit negotiations.

Malaysia’s message is unambiguous: the government is no longer subsidizing foreign final-assembly jobs. Only manufacturers prepared to weld, paint, and install battery management systems on Malaysian soil will continue to receive the fiscal support that makes EVs affordable in a price-sensitive market. The policy also sends a clear signal to neighboring Indonesia and Thailand that Kuala Lumpur intends to capture the lion’s share of ASEAN EV production investment, even if it means sacrificing short-term consumer choice.

Pro Tip for Fleet Buyers and Consumers: If you are considering an imported EV from any of the affected brands, finalize your purchase before the 2026 enforcement window closes. Remaining CBU stock will likely appreciate in value as supply freezes, but post-ruling support networks may deteriorate if brand representatives withdraw from the country entirely. Prioritize models with established local service centers and verified parts warehouses.

Global Implications and Market Realignment

This policy shift places Malaysia in a unique position within ASEAN. While Thailand and Indonesia have also pushed for local EV assembly, neither has executed such a sudden elimination of CBU incentives. The ruling will force regional headquarters to reroute investment dollars toward Kuala Lumpur or abandon the peninsula entirely. Global automakers now face a cascading decision matrix: absorb the cost of a Malaysian plant, partner with an existing domestic assembler, or forfeit a market of over 33 million consumers.

For consumers cross-shopping in Singapore, Indonesia, or Thailand, the divergence will be stark. Models available across ASEAN as CBU units will become Malaysia-specific variants or disappear entirely. Resale values for pre-2026 imported EVs may fluctuate based on perceived parts availability, creating a two-tier market of supported and unsupported electric vehicles. Insurance and financing providers are already reassessing risk models for brands with uncertain long-term presence.

Frequently Asked Questions

Does the ruling affect hybrid vehicles or only fully electric models?

The directive targets fully electric CBU vehicles specifically. Hybrid and plug-in hybrid models currently fall under separate harmonized tariff schedules and are not subject to the same assembly mandate at this time. However, industry observers expect similar localization pressure to extend to electrified hybrids by 2028.

Can consumers still import a Tesla or BYD privately after 2026?

Private importation remains technically possible but economically prohibitive. Without Approved Permits and duty exemptions, import tariffs, sales tax, and excise duties can inflate the landed cost by over 100 percent. A model priced at $35,000 USD under the previous scheme could effectively cost $70,000 USD or more after fees.

Which brands are already safe because they have local assembly?

Perodua and Proton’s upcoming EV lines are insulated through national partnerships. Mercedes-Benz has already established selected CKD capacity for certain EQ models. Any manufacturer with an operational assembly line certified by MITI prior to the ruling will retain its incentive structure, provided local content thresholds are met.

Will used CBU EV prices increase because of this policy?

Yes. Scarcity of new imported units typically drives secondary-market premiums for existing stock. Buyers should factor in potential battery degradation and the availability of over-the-air software support before paying inflated prices for out-of-production CBU imports.

How does this compare to EV policies in the United States or European Union?

Unlike the Inflation Reduction Act in the United States, which ties consumer tax credits to North American assembly gradually, Malaysia’s ruling is an immediate hard stop. The European Union’s emissions regulations focus on manufacturer fleet averages rather than import structure. Malaysia’s approach is closer to an outright trade barrier disguised as industrial policy, making it one of the most aggressive localization pushes globally.

Conclusion

MITI’s 2026 CBU EV ruling is not a policy adjustment; it is a market purge. Brands that built their Malaysian presence on imported fully built units must now commit to heavy domestic investment or surrender their market share to competitors with deeper local roots. For buyers, the window to acquire internationally assembled electric vehicles is closing rapidly. Share your perspective in the comments: which brand do you think will be first to announce a Malaysian factory, and which will quietly exit the stage?